I Will See to the Continuous Cashflow

Cash Flow Statement

A reconciliation of the cash generated and used in a period

What is the Cash Flow Statement?

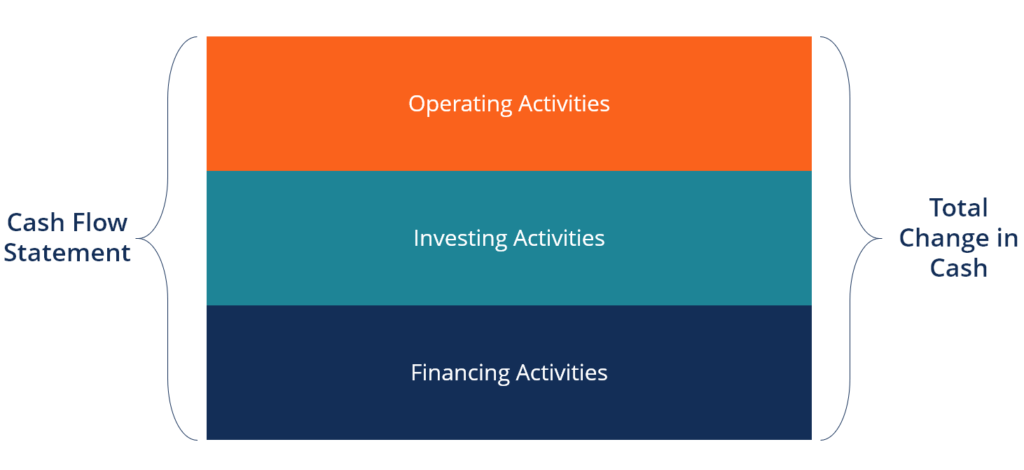

A Cash Flow Statement (also called the Statement of Cash Flows) shows how much cash is generated and used during a given time period. It is one of themain financial statements analysts use in building a three statement model. The main categories found in a cash flow statement are (1) operating activities, (2) investing activities, and (3) financing activities of a company and are organized respectively.

The total cash provided from or used by each of the three activities is summed to arrive at the total change in cash for the period, which is then added to the opening cash balance to arrive at the cash flow statement's bottom line, the closing cash balance.

One of the primary reasons cash inflows and outflows are observed is to compare the cash from operations to net income. This comparison helps company management, analysts, and investors to gauge how well a company is running its operations. The cash flow statement reflects the actual amount of money the company receives from its operations.

The reason for the difference between cash and profit is because the income statement is prepared under the accrual basis of accounting, where it matches revenues and expenses for the accounting period, even though revenues may actually not have yet been collected and expenses may not have yet been paid. In contrast, the cash flow statement only recognizes cash that has actually been received or disbursed.

Image: CFI Financial Modeling Courses.

Download the Free Template

Enter your name and email in the form below and download the free template now!

How to Set Up the Cash Flow Statement?

Below is a breakdown of each section in a statement of cash flows. While each company will have its own unique line items, the general setup is usually the same. This guide will give you a good overview of what to look for when analyzing a company.

#1 Operating Cash Flow

The cash flow statement begins with Cash Flow from Operating Activities. It starts with net income or loss, followed by additions to or subtractions from that amount to adjust the net income to a total cash flow figure. What is added or subtracted are changes in the account balances of items found in current assets and current liabilities on the balance sheet, as well as non-cash accounts (e.g., stock-based compensation). We then arrive at the cash version of a company's net income.

Net Earnings

This amount is the bottom line of an income statement. Net income or earnings shows the profitability of a company over a period of time. It is calculated by taking total revenues and subtracting from them the COGS and total expenses, which includes SG&A, Depreciation and Amortization, interest, etc.

Plus: Depreciation and Amortization (D&A)

The value of various assets declines over time when used in a business. As a result, D&A are expenses that allocate the cost of an asset over its useful life. Depreciation involves tangible assets such as buildings, machinery, and equipment, whereas amortization involves intangible assets such as patents, copyrights, goodwill, and software. D&A reduces net income in the income statement. However, we add this back into the cash flow statement to adjust net income because these are non-cash expenses. In other words, no cash transactions are involved.

Less: Changes in working capital

Working capital represents the difference between a company's current assets and current liabilities. Any changes in current assets (other than cash) and current liabilities affect the cash balance in operating activities.

For instance, when a company buys more inventory, current assets increase. This positive change in inventory is subtracted from net income because it is seen as a cash outflow. It's the same case for accounts receivable. When it increases, it means the company sold their goods on credit. There was no cash transaction, so accounts receivable is also subtracted from net income.

On the other hand, if a current liability item such as accounts payable increases, this is considered a cash inflow because the company has more cash to keep in its business. This is then added to net income.

Cash from operations

When all the adjustments have been made, we arrive at the net cash provided by the company's operating activities. This is not a replacement for net income, but rather a summary of how much cash is generated from the company's core business.

#2 Investing Cash Flow

This category on the statement of cash flows is referred to as Cash Flow from Investing Activities and reports changes in capital expenditures (CapEx) and long-term investments. CapExcan refer to the purchase of property, plant, or equipment assets. Long-term investments may include debt and equity instruments of other companies. Another important item found here is acquisitions of other businesses. A key to remember is that a change in the long-term assets in the balance sheet is reported in the investing activities of the cash flow statement.

Investments in Property and Equipment

These CapEx investments might mean purchases of new office equipment such as computers and printers for a growing number of employees, or the purchase of new land and a building to house business operations and logistics of the company. These items are necessary to keep the company running. These investments are a cash outflow, and therefore will have a negative impact when we calculate the net increase in cash from all activities. Learn how to calculate CapEx with the CapEx formula.

Cash from investing

This is the total amount of cash provided by (used in) investing activities. In our example, we have a net outflow for each and every year.

#3 Financing Cash Flow

This category is also called Cash Flow from Financing Activities and reports any issuance or repurchases of stocks and bonds of the company, as well as any dividend payments it makes. The changes in long-term liabilities and stockholders' equity in the balance sheet are reported in financing activities.

Issuance (repayment) of debt

A company issues debt as a way to finance its operations. The more cash it has, the better, as it will be able to expand rapidly. Unlike equity, issuing debt doesn't grant any ownership interest in the company, so it doesn't dilute the ownership of existing shareholders. The issuance of debt is a cash inflow, because a company finds investors willing to act as lenders. However, when these investors are paid back, then the debt repayment is a cash outflow.

Issuance (repayment) of equity

This is another way of financing a company's operations. Unlike debt, equity holders have some ownership stake in the business in exchange for money given to the company for use. Future earnings must be shared with these equity holders or investors. Issuance of equity is an additional source of cash, so it's a cash inflow. Conversely, an equity repayment is a cash outflow. This is buying back, through cash payment, the equity from its investors and thereby increasing the stake held by the company itself.

Cash from financing

This is also called the net cash provided by (used in) financing activities. The cash from financing is calculated by summing up all the cash inflows and outflows related to changes in long-term liabilities and shareholders' equity accounts.

#4 Cash Balance

The last section on the statement of cash flows is a reconciliation of the total cash position, which connects to the balance sheet. This is the final piece of the puzzle when linking the three financial statements.

Net Increase (decrease) in Cash and Closing Cash Balance

Once we have all net cash balances for each of the three sections of the cash flow statement, we sum them all up to find the net cash increase or decrease for the given time period. We then take this amount and add it to the opening cash balance to eventually arrive at the closing cash balance. This amount will be reported in the balance sheet statement under the current asset section.

Opening cash balance

The opening cash balance is last year's closing cash balance. We can find this amount from last year's cash flow statement and balance sheet statement.

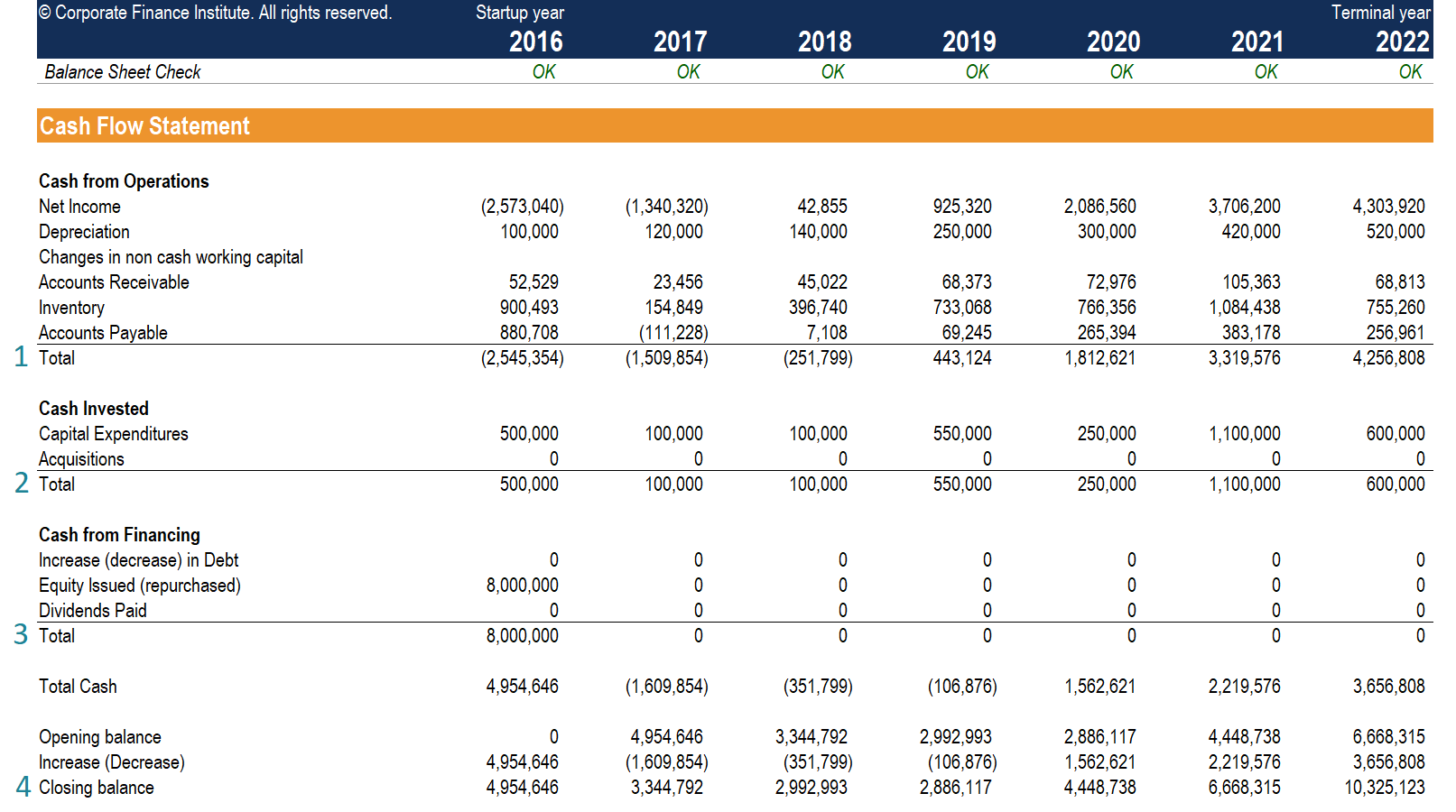

Real-Life Example of a Cash Flow Statement (Amazon)

Below is an example of Amazon's 2016 statement of cash flows. As you can see by the orange rectangles, there are three clear sections that add to the total change and end of period cash position. For a closer look, you can download Amazon's financial statements here, or you can check out CFI's Advanced Financial Modeling Course on Amazon.

How to Build a Statement of Cash Flows in a Financial Model

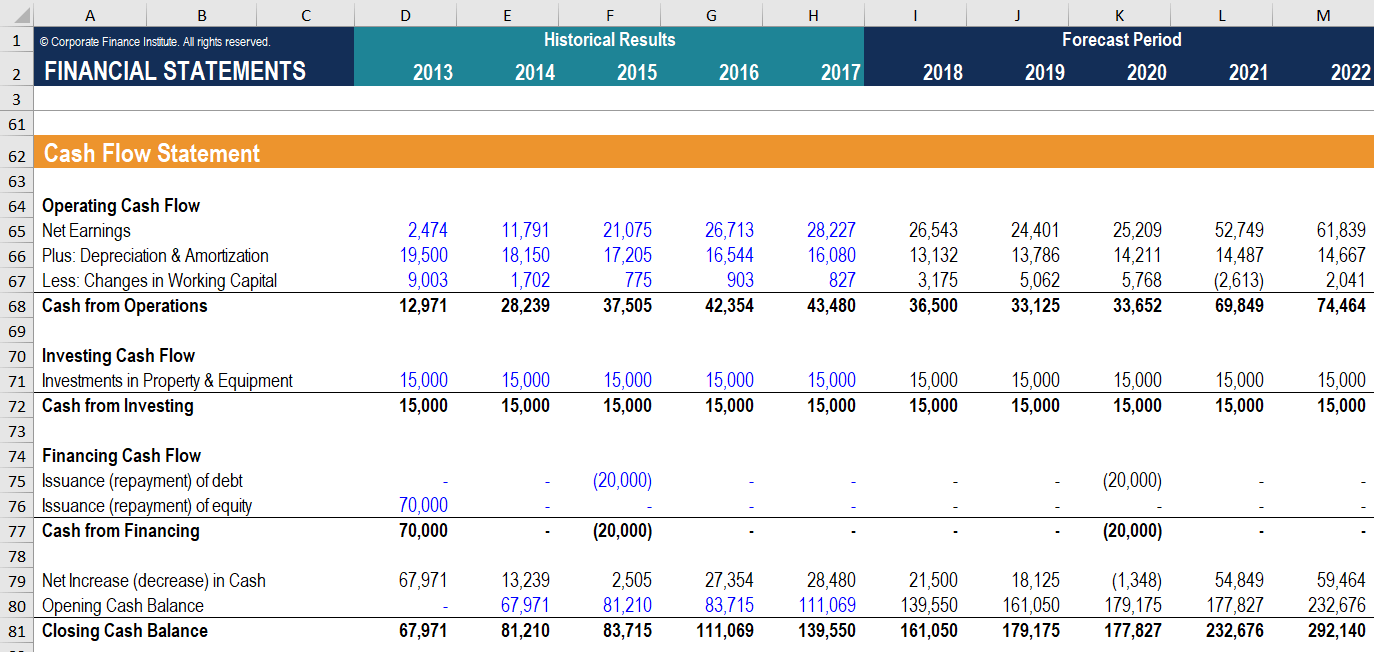

A cash flow statement in a financial model in Excel displays both historical and projected data. Before this model can be created, we first need to have the income statement and balance sheet statement models built in Excel, since their data will ultimately drive the cash flow statement model.

Image: CFI Financial Modeling Courses.

As we have seen from our financial model example, it shows all the historical data in a blue font, while the forecasted data appears in a black font. The figure below just serves as a general guideline as to where to find historical data to hardcode for the line items. Additionally, it shows where we find, in the financial model, the calculated or reference data to fill up the forecast period section.

When all three statements are built in Excel, we now have what we call a "Three Statement Model". Below is a summary of how to build a statement of cash flows in Excel.

| Line Items | Historical Results (Annual Report) | Forecast Periods (Model) |

|---|---|---|

| Net Earnings | Income Statement | Income Statement |

| Depreciation & Amortization | Income Statement | PP&E Schedule |

| Changes in Working Capital | Balance Sheet | Working Capital Schedule |

| Capital Expenditures | Balance Sheet | PP&E Schedule |

| Debt Issuance | Balance Sheet | Debt Schedule |

| Equity Issuance | Balance Sheet | Equity Schedule |

| Opening Cash Balance | Prior Period Balance Sheet | Prior Period Balance Sheet |

Video Explanation of the Cash Flow Statement

Watch this short video to quickly understand the main concepts covered in this guide, including what the cash flow statement is, how it works, and most importantly, why it matters to finance professionals.

Additional Resources

Thank you for reading CFI's guide to understanding how the cash flow statement works. To continue learning and advancing your career as a professional financial analyst, these additional CFI resources will be helpful:

- Balance Sheet Overview

- Income Statement Overview

- What is a Financial Model?

- Top Financial Analyst Certifications

juarezcoatseardeas.blogspot.com

Source: https://corporatefinanceinstitute.com/resources/knowledge/accounting/cash-flow-statement%E2%80%8B/

0 Response to "I Will See to the Continuous Cashflow"

Postar um comentário